Phone:

(920) 544-0576

Blog Layout

Avoiding Social Security's Tax Trap

Eric Sajdak • Feb 14, 2020

Do you know when Social Security was signed into law, the first pamphlet they gave to retirees said Social Security is not taxed and never will be?

Well, hopefully, no one took congress at their word. A lot has changed since then, and now Social Security is taxed a few different ways.

For simplicity's sake, we are going to talk about taxes in terms of a married couple (the numbers in this article will change slightly for an individual). Taxes on Social Security can get quite complicated.

This article is a 1,000-foot overview of Social Security and its taxability. If you are interested in learning more about the gritty details of how Social Security is taxed, I'd recommend you attend our Maximizing Social Security class.

The Tax Trap Impact

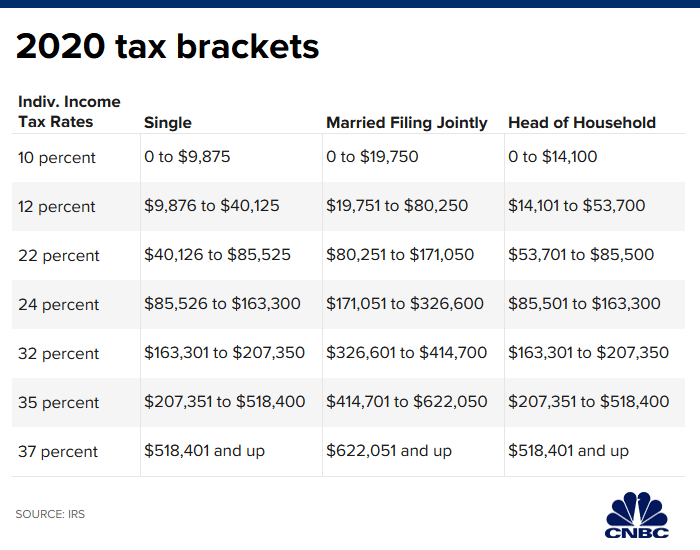

The tax tables, while you are working and earning income from a job, are straightforward. We have a graded, marginal tax system where each dollar is taxed based on what bracket that dollar falls into. Below is the 2020 marginal tax bracket. We'll call it the Worker's Tax System:

Pretty straightforward.

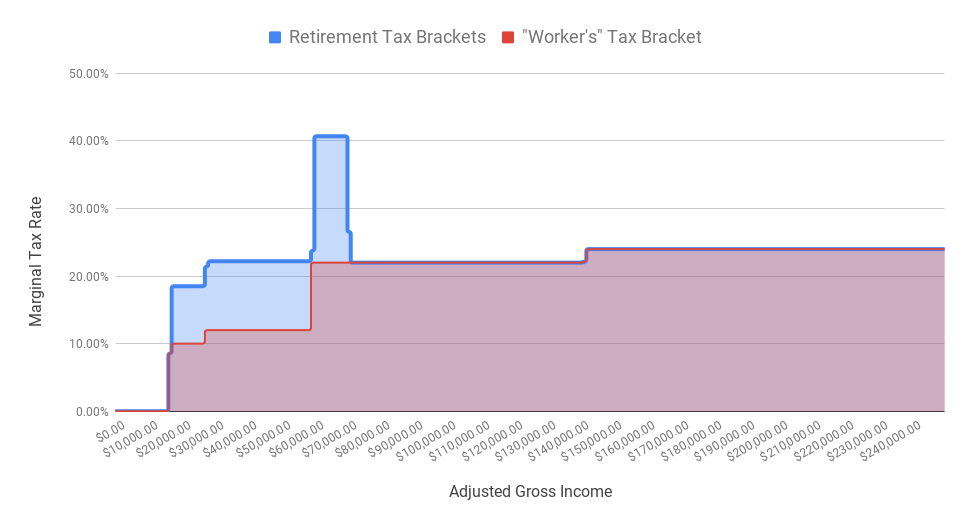

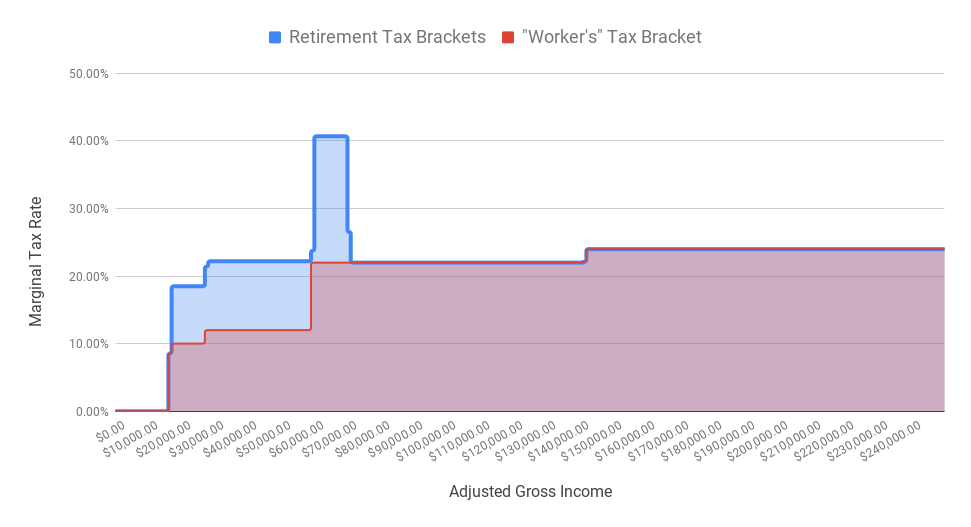

Once you enter retirement and turn on Social Security, you can throw this entire tax table out the window. The complex way in which Social Security is taxed creates a new tax system for retirees.

As your taxable income increases, more of your Social Security benefit becomes taxable (up to 85%).

Below is the Retiree's Tax System assuming the couple here has $64,000 of combined Social Security benefit:

Two areas on the graph create a tax trap for retirees. The first trap is between taxable income levels of $17,000 and $59,000. The marginal rate throughout this range is 83-85% higher than the workers tax system.

The second tax trap range is between $60,000 and $69,000. Once again, we see a marginal rate increase from 22% to 40.70% (85% higher!). Each of these two tax trap zones cost you significant taxes each year. For the average retiree, the added tax from these traps will cost the average married couple approximately $5,000 per year in added taxes!

Here is where the value of a retirement income specialist comes in.

Both of these tax traps are avoidable with the right strategies. The result, you save approximately $5,000 per year in taxes.

What Causes the Tax Trap?

In short, the more you pull from taxable accounts and traditional retirement accounts, the more of Social Security is taxed. As more Social Secuirty is taxed, your marginal rates jumps significantly.

Distributions from Roth IRA's, however, are tax-free and, therefore, not included in taxable income. This is why an optimized withdrawal strategy is so crucial for retirees entering retirement. Roth money can you help you avoid these Tax Traps!

The problem with that? Most retirees don't have significant Roth assets to allow for large withdrawals.

This is where Roth conversions and partial Roth Conversions become key. We'll save that discussion for another article, however.

So, what's the big takeaway from this article?

Your Retirement Tax System is one of the most important things to know in retirement planning.

It is the catalyst for numerous decisions you will have to make through retirement from withdrawal strategy to conversions and everything in between.

CRITICAL FACT: Everyone's retirement tax table will look different based on your Social Security benefit! Don't use the example table in this article to plan for your situation.

If you're a retiree or a soon-to-be retiree, we highly recommend sitting down with an income specialist to help avoid the Social Security Tax Trap. Every year, $5,000 you don't pay to Uncle Sam is $5,000 that stays invested, stays earning interest for your retirement.

Want Safeguard to show you what your Retirement Tax Brackets look like? Request a strategy session. You can do so by calling (920) 544-0576 or by clicking here.

"If I delay my Social Security benefit, at what age would I breakeven versus simply filing at 62?" We field this type of question frequently from retirees. The Social Security system allows you to file anytime between 62 and age 70. At first glance, filing at 62 seems to make the most sense. After all, there are 12 months in a year and eight years between ages 62 and 70—That's 96 months of monthly paychecks that you wouldn't be getting if you delayed. However, you get penalized for taking your benefit early. Below is a diagram showing the penalties and delayed credits for someone whose Full Retirement Age is 66:

Lately I’ve been getting asked how I was able to “Call the Bottom” in late March. I want to make something clear: I didn’t. If you go back and look at the article from March 16th or read the email I sent out to subscribers on the 26th, (pure dumb luck), I ran a bad case, a best case, and a base case valuation on the S&P 500. I arrived at a base case valuation of 2,950, and at the time the S&P was hovering around 2,300, so we started recommending clients initiate buying plans. These plans did not mean “This is the bottom” or “Go all in.” Far from it. Many of our clients were buying several days before the precise bottom, and several days and weeks after. Regardless of how clearly I try to make this point (that we simply were buying something the math said was likely cheap) this morning my inbox is chock full of people asking what I think about valuations now. Are we in a bubble? Is the market ahead of the fundamentals? Are we going to double dip? Will the market crash? Will we need a second stimulus? Maybe. I have no idea. Here’s what I know, when you accumulate all of the available earnings estimates and make a conservative estimate of fair value, you end up with a fair value of about 3,060 on the S&P 500. As I type this we sit at 3,080. Regardless of whether the number is 2,950 or 3,060 or 3,080 or 3,150, any way you slice it, we’re at fair value, now. Analyst Earnings Estimates:

It is your right as an American to (legally) pay the least amount in taxes that you owe—nothing more, nothing less. But in recent years, Congress has made a concerted effort to shift the IRS code and levy you with taxes you didn't even know you were paying. We call these "Stealth Taxes." These changes are never talked about by your congressman (or woman). They lie deep within the tax code and can potentially cost you significantly unless you learn about how to avoid them. In this article, we cover three of those "Stealth Taxes" and what you can do to minimize or avoid them altogether.

Contact Our Team

By using this website, you understand the information being presented is provided for informational purposes only and agree to our Terms of Use and Privacy Policy. Safeguard Wealth Management relies on information from various sources believed to be reliable, including clients and third parties, but cannot guarantee the accuracy and completeness of that information. Nothing in this communication should be construed as an offer, recommendation, or solicitation to buy or sell any security. Additionally, Safeguard Wealth Management or its affiliates do not provide tax advice and investors are encouraged to consult with their personal tax advisors.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. Please see our Full Disclosure for important details.

Safeguard Wealth Management is a Registered Investment Advisor with the SEC.