Phone:

(920) 544-0576

Blog Layout

What is Your Plan From Here?

Eric Sajdak • Mar 20, 2020

Due to everything going on with the Coronavirus and financial markets, the spectrum of questions we are fielding right now is broad.

From:

"Should I be taking all of my money out of the market right now? It seems like this could get a lot worse!"

To:

"I have had cash on the sideline in case of a crash, are stocks cheap? Should I deploy that money and get back into the market?"

And on a grander scale:

"What does this mean for my retirement? Does my plan change?"

From a valuation standpoint, Tony wrote an excellent article showing what we should expect over the intermediate to long term.

Click here to read it.

In this article, I am going to explore each of the questions above and talk you through different ways to plan for the Coronavirus impact.

I don't mean a plan from a health standpoint; I'll leave that up to the doctors (and those who are playing doctors on Facebook)

A Plan For Coronavirus

I cannot say this enough; the worst plan is having no plan. The second worse plan is an irrational one. One based on emotion, rumors heard from co-workers, Facebook friends, or a plan driven by fear.

Question 1: "Should I get out of the stock market completely?"

Step back from the Coronavirus pandemic completely. In the worst-case scenario, this will be a national tragedy. I don't want to downplay that in any way. Tragedies are real, and they will be felt close to home if it gets to that point.

However, as bad as the Coronavirus is, it is temporary. The social distancing and quarantining will cease at some point in the future. When? That is yet to be determined. But life will return to normal.

That also means the economy and stock market will return to normal as well.

No one, and I mean no one, knows when we will see the stock market "bottom".

Maybe it has already happened, or perhaps the market will fall to -50%. If we map out all the possibilities, statistically, you have already felt most of the pain. Which means it would be unwise to exit now.

Exiting the stock market now opens the flood gates for questions:

- Are you going to take everything out of the market or just a portion? How will you determine?

- When will you invest back in?

- Will you try to invest back in when things get cheaper? When is cheap enough? If it never does, are you just going to sit on the sidelines?

- Will you try to invest when things rebound? What is your definition of rebound? What if it rebounds and turns lower? Will you buy and hold from there or sell?

- Have you thought through all the potential scenarios from here?

- Separate and identify where the emotion to sell is coming from. Did you see all the toilet paper and rice sold out at the local Costco or Walmart? Did that send you into thinking this is the start of a mini-apocalypse? Separate fact from feeling. What are the facts?

Why are you exiting anyway? If you were taking too much risk before this all, then so be it. We can't go back in time. Learn from it and move forward.

Now is not the time to exit, even if the stock market falls from here.

Question 2: "Should I invest the cash I have had sitting on the sidelines right now?"

The market is down; you have cash sitting on the sidelines, is now the time to deploy it?

Statistically yes. Again, check out

Tony's article to see a fundamental analysis of where the market is.

But there are a few other things to consider.

Are you going to lump-sum (all at once) or periodically invest that money?

Most investors don't have the stomach for a lump sum. The market is "cheap" right now, but it can go down further and become cheaper. Panic increases exponentially with every -1% drop.

For example, let's say you lump summed that money right now. A week from now, the market improves by +10% from right now. You're feeling pretty smart. The market reverses and falls by -20% (-10% from here. Approx. -40% overall.) You go from feeling brilliant to feeling like an idiot (don't worry, you're not). Every radio show, news program, social media post, etc. is about how bad this all is going to get.

Do you have the stomach to sit through that all?

We advise a more caution-first approach. Use a concept called Dollar Cost Averaging to your benefit. But have a plan.

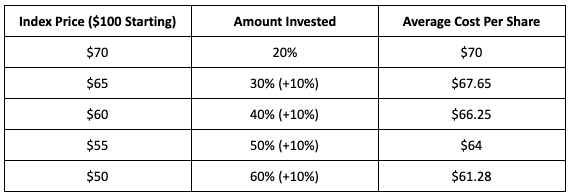

For instance, the plan might be:

- Today, I am going to invest 20% of my cash.

- Every -5% drop from here, I am going to invest 10% more into the market.

Dollar-cost averaging “protects” you as the market falls. What looks like a $20 loss from your initial purchase is actually only an $11.28 loss per share. You’re upside increases as the market rebounds as well.

You and your advisor can decide on the parameters. Move forward with caution. Don’t jeopardize your overall plan in search of a bargain.

The stock market is the single greatest wealth creator in the world but also the single greatest wealth destroyer.

Make sure you're on the right side.

Question 3: "What does this mean for your retirement?"

This is the most critical question those 55+ should be asking.

The answer will vary for everyone.

If you can't or don't get a numerical answer to this question from your advisor, I would highly recommend getting a second opinion.

What do I mean?

When we run an investor's retirement plan, we give them a probability of success score, like 92%. This means that in 92% of cases, the investor has enough money to make it to the end of retirement (this is based on 1,000 different simulations of their retirement).

The U.S. Stock Market is down almost -30% as of writing this. For the majority of investors, especially on the goal line of retirement, this drop will materially affect their retirement. But by how much?

I don't mean to "toot our own horn" and say if your advisor doesn't plan like we do, you should switch advisors. I'm merely saying that if you ask your advisor what your retirement looks like right now and they aren't able to give you a math-based answer, I would question whether they even know the answer.

You deserve more than answers like, "Don't worry, stay the course; everything will be fine."

An example of a good answer would be,

“Bill, we re-ran your probability of success. Prior to this drawdown, your probability of success was 97%. It currently is 92%. That might seem like a big hit but remember, the money we put in stocks we won’t need for another 5 years, so we have time built in for a recovery. How are you and Nancy feeling? There are a few tax strategies we should be taking advantage of in a time like this though...”

Which answer would help you sleep better at night?

Almost no matter who you are, you can be making changes to improve your long-term situation. Here are a few:

- Moving bond risk off the table for better alternatives

- Tax Loss Harvesting in Taxable Accounts

- Roth Conversions

- Refinance Your Mortgage or Restructure High-Interest Debt

- Start Dollar Cost Averaging into the Financial Markets

In a time of high panic, I hope this article helped provide a bit of clarity and answer some of the most pressing questions on your mind.

"If I delay my Social Security benefit, at what age would I breakeven versus simply filing at 62?" We field this type of question frequently from retirees. The Social Security system allows you to file anytime between 62 and age 70. At first glance, filing at 62 seems to make the most sense. After all, there are 12 months in a year and eight years between ages 62 and 70—That's 96 months of monthly paychecks that you wouldn't be getting if you delayed. However, you get penalized for taking your benefit early. Below is a diagram showing the penalties and delayed credits for someone whose Full Retirement Age is 66:

Lately I’ve been getting asked how I was able to “Call the Bottom” in late March. I want to make something clear: I didn’t. If you go back and look at the article from March 16th or read the email I sent out to subscribers on the 26th, (pure dumb luck), I ran a bad case, a best case, and a base case valuation on the S&P 500. I arrived at a base case valuation of 2,950, and at the time the S&P was hovering around 2,300, so we started recommending clients initiate buying plans. These plans did not mean “This is the bottom” or “Go all in.” Far from it. Many of our clients were buying several days before the precise bottom, and several days and weeks after. Regardless of how clearly I try to make this point (that we simply were buying something the math said was likely cheap) this morning my inbox is chock full of people asking what I think about valuations now. Are we in a bubble? Is the market ahead of the fundamentals? Are we going to double dip? Will the market crash? Will we need a second stimulus? Maybe. I have no idea. Here’s what I know, when you accumulate all of the available earnings estimates and make a conservative estimate of fair value, you end up with a fair value of about 3,060 on the S&P 500. As I type this we sit at 3,080. Regardless of whether the number is 2,950 or 3,060 or 3,080 or 3,150, any way you slice it, we’re at fair value, now. Analyst Earnings Estimates:

It is your right as an American to (legally) pay the least amount in taxes that you owe—nothing more, nothing less. But in recent years, Congress has made a concerted effort to shift the IRS code and levy you with taxes you didn't even know you were paying. We call these "Stealth Taxes." These changes are never talked about by your congressman (or woman). They lie deep within the tax code and can potentially cost you significantly unless you learn about how to avoid them. In this article, we cover three of those "Stealth Taxes" and what you can do to minimize or avoid them altogether.

Contact Our Team

By using this website, you understand the information being presented is provided for informational purposes only and agree to our Terms of Use and Privacy Policy. Safeguard Wealth Management relies on information from various sources believed to be reliable, including clients and third parties, but cannot guarantee the accuracy and completeness of that information. Nothing in this communication should be construed as an offer, recommendation, or solicitation to buy or sell any security. Additionally, Safeguard Wealth Management or its affiliates do not provide tax advice and investors are encouraged to consult with their personal tax advisors.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. Please see our Full Disclosure for important details.

Safeguard Wealth Management is a Registered Investment Advisor with the SEC.